王天财

5

tips

HDB Homeowners Should Know Before Upgrading

MAGAZINE TITLE

CONTENTS

1

Understand the Difference Between HDB Loans & Bank Loans

2

Be Financially

Prudent

3

Do Not Take

ABSD Remission

For Granted

4

Take Note That the Property You Are Upgrading to Will Affect the Future Asset Progression

5

Keep In Mind That Upgrading Now Is Always Better Than Later

Tip # 1

Understand The Difference Between HDB Loan & Bank Loan

_PNG.png)

HDB Homeowners

may be unfamiliar

with Bank

Loans if they

financed

their flat

with a

HDB Loan

Which Loans can

you apply for when buying property?

HDB

Loan

HDB

Loan

HDB

Flats

Executive

Condos

Private Homes

Source: Housing development boards, monetary authority of Singapore

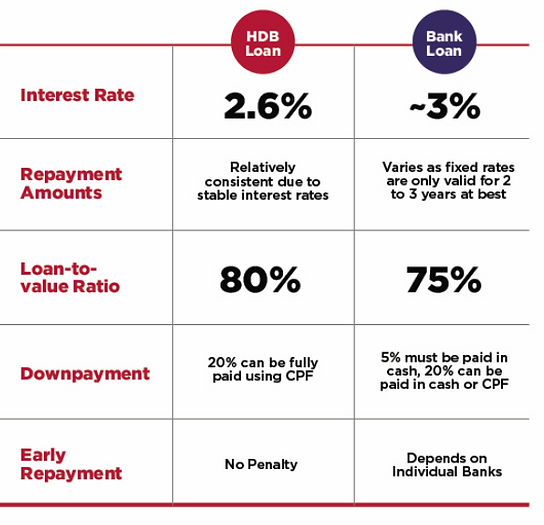

The interest

rate for a

HDB loan is

typically at

2.6%* while

bank loan

interest rates

fluctuate**.

"HDB loan rates is 0.19% above CPF OA rate of 2.5%

Flood ratos are only valid for 2-3 years for a bank loan.

Source: Housing Development Board, Singapore Banks

A quick Summary

Assumptions based on 3-mth Compoounded SORA + 1% as of the 1 September 2022 source. Monetary authority of Singapore, Housing development board, ERA.

You may

not need

to fork out

any cash for

HDB loans

but bank

loans require

compulsory

5% cash.

Note: Based on best LTV an tenure terms.

Your monthly

installments

may not be

the same due

to variable

interest rates

for bank

loans

Tip #2

Be

Financially

Prudent

_PNG.png)

Remember

to exercise

financial

prudency

when

upgrading.

Always have

enough cash

and CPPF

OA funds to

COver down

payments

and monthly

repayments.

Do l have enough

money to upgrade?

Case Study

Note: The purchase price of BTO based on Real BTO BTO project launched in 2012.

* Include CPF OA not returned yet, excluding all expenses.

Is $440,000

enough

for me tO

upgrade to a

$1,200,000

condo?

Using sales

proceeds to upgrade.

NOTE: excluding miscellaneous expences

SOURCE: Inland revenue Authority of Singapore

$440,000

>

$333,000

PROCEEDS MORE THAN DOWNPAYMENT!

If your HBD sale proceeds exceed your condo upfront payment, you can definitely afford a $1,200,000 condo!

NOTE: you must fill TDSR requirements

If you have extra savings it can even go towards funding your home renovations

_PNG.png)

Tip # 3

Do not Take ABSD Rermission For Granted

ABSD

remission

is only

applicable

for a joint

purchase

by married

couples

At least one Singapore

CItlzen Spouse

More information can be

found at Inland Revenue

Authority of Singapore.

Remember

to sell your

existing HDB

flat within 6

months.

Otherwise

your ABSD

will not be

refunded.

Are you willing to

take the risks?

Scenario 1: Seller is flexible In his selling price

Low Risk

Scenario 2: Seller is fixated On waiting for the "right" buyer and Is

Inflexible about his selling price.

High Risk

NOTE: OTP stands for Options to Purchase

Tip #4

Take Note

That the

Property

You Are

Upgrading to

Will Affect

Future Asset

Progression

Every

property has

a 'waiting

time' before

it can be sold

in the open

market.

How long is the

'waiting time'?

Shorter

Waiting Time

Longer

Waiting Time

Tip #5

Keep In

Mind That

Upgrading

Now Is

Always

Better

Than Later

Private home prices

are becoming more

and more expensive...

New launch condo prices have grown 106.8%

since 10 years ago.

Resale condo prices have grown 39.6% since

10 years ago.

Source: Urban redevelopment authority

This is happening

right now...

FDI stands for foreigh direct investment

New launch

prices are

trending

upwards

because

of cost

pressures.

The longer

you delay,

the higher

new launch

prices will

become.

The benefits of

upgrading early.

1

Lock-in a lower entry

price for higher

potential profits.

2

The younger you are,

the longer the loan

tenure which implies

lower mortgage

repayments.

Conclusion

There are many

differences

between private

property

ownership &

HDB ownership,

ranging from

loans types

to financial

responsibilities.

It is possible

to upgrade

from a HDB

to condo

so long as

the sales

proceeds can

cover most of

your condo's

down

payment.

Tax reliefs

such as

ABSD

remission

are subject

to certain

criteria

set by the

government.

Don't take

too long to

find the best

offer before

you sell your

HDB flat.

Need

help with

planning

your asset

progression?